Governments and private firms can both issue gold bonds, but not all gold bond programs are structured the same way.

In 2015, India launched its Sovereign Gold Bond (SGB) scheme in an effort to reduce demand for imported physical gold. The program initially attracted significant investor interest by offering exposure to gold prices alongside a fixed interest payment.

Yet despite its popularity, the scheme was discontinued less than a decade later1.

Why did it fail?

And what lessons does its failure offer investors interested in earning a return on their gold?

Why did India create sovereign gold bonds?

India is one of the world’s largest consumers of gold.

Because most of that gold must be imported, growing gold demand can increase the country’s need for U.S. dollars. Importers typically purchase gold in dollars, which can place pressure on India’s foreign exchange reserves and, at times, the value of the rupee.

To address this challenge, the Indian government launched the Sovereign Gold Bond (SGB) scheme in 2015.

The idea was straightforward: instead of purchasing physical gold, investors could buy government-issued bonds linked to the price of gold.

If enough investors chose bonds instead of bullion, it could reduce gold imports while still satisfying investor demand for gold exposure—the government hoped.

How did sovereign gold bonds work?

The Reserve Bank of India (RBI) issued SGBs on behalf of the Indian government.

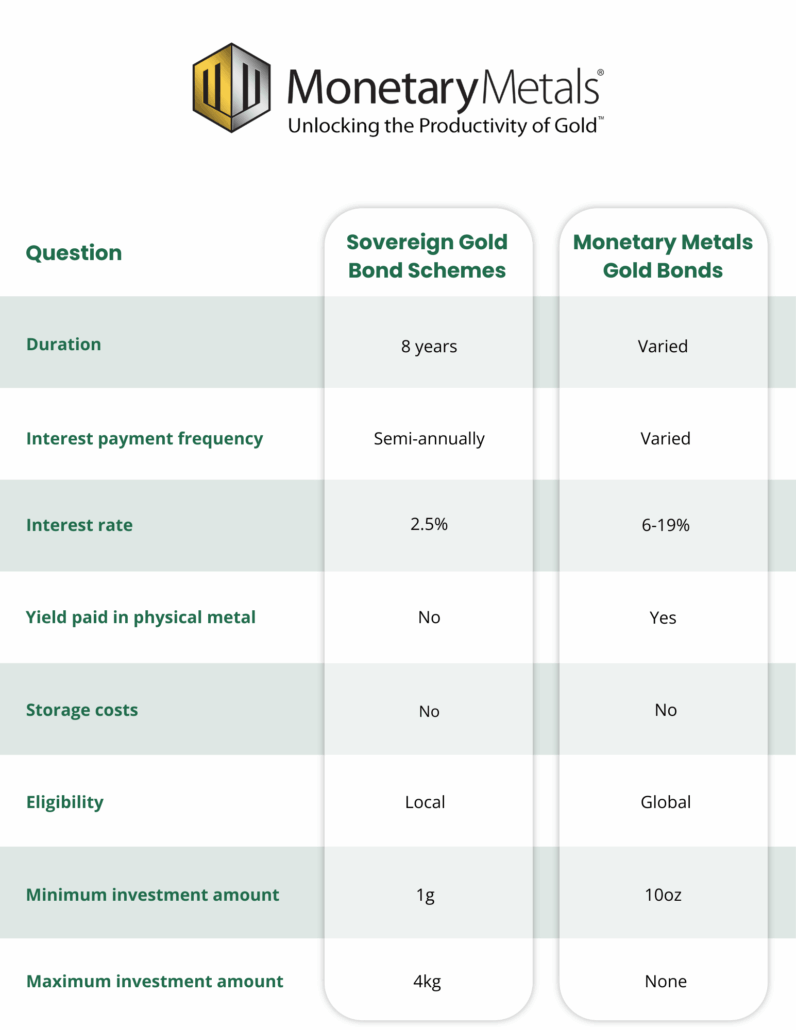

Investors purchased bonds denominated in grams of gold and received a fixed annual interest payment in rupees. At maturity, investors received the rupee value of the gold represented by their bonds.

Key features of SGBs included:

- Gold-linked principal: Investors purchased bonds representing a fixed quantity of gold.

- Fixed interest rate: The bonds paid 2.5% annual interest, denominated and paid in rupees.

- Government guarantee: Principal and interest obligations were backed by the Indian government.

- Cash redemption: Investors received cash at maturity rather than physical gold.

- Tax benefits: Capital gains tax exemptions were available for long-term holders.

For many investors, the program offered an attractive combination of gold price exposure and income.

However, several structural challenges emerged over time.

Why was the Sovereign Gold Bond scheme discontinued?

Although the program attracted investors, three major issues limited its long-term success:

- Reducing gold demand proved difficult.

- Rising gold prices increased government liabilities.

- The yield wasn’t generated by productive use of gold.

Reducing gold demand proved difficult.

The first challenge was cultural.

As we mentioned, one of the government’s central goals was to reduce demand for imported physical gold.

That proved easier said than done.

In India, gold often serves purposes that extend far beyond investment. Jewelry is deeply embedded in family traditions, cultural celebrations, and wealth preservation.

For many families, converting jewelry into a financial product can be difficult for practical, emotional, and cultural reasons.

As a result, the government faced a difficult task: persuading gold owners to give up physical ownership in a country where physical ownership itself is often part of the value proposition.

Rising gold prices increased government liabilities.

The second challenge was financial.

As gold prices rose, the government’s obligations to bondholders increased.

While investors benefited from higher gold prices, the program became increasingly expensive for the issuer.

Over time, these growing liabilities made new bond issuances less attractive from the government’s perspective.

The yield wasn’t generated by productive use of gold.

The third challenge was structural.

Unlike traditional lending or gold-backed financing arrangements, the government wasn’t deploying gold into productive economic activity to generate returns.

The 2.5% interest payments were funded by taxpayers rather than earned through gold leasing, lending, manufacturing, mining, or other productive uses of gold.

In other words, the program provided investors with a yield, but there was no underlying mechanism that generated that yield from the gold itself.

Generally, sustainable investment returns depend on productive economic activity. Without that foundation, the program became increasingly difficult to justify as costs rose.

A different approach: Gold bonds backed by productive use

A gold bond can be structured in more than one way.

India’s Sovereign Gold Bond program provided investors with gold exposure and a fixed yield, but that yield was funded by the government.

Alternatively, a gold bond can also be structured as a form of gold-denominated credit.

In this model, gold functions as capital: investors lend gold or gold-linked capital to borrowers who can use it in commercial activity.

For example, a gold-using business may borrow gold to finance production, manage inventory, or reduce exposure to fiat currency fluctuations.

The return paid to investors is then connected to the borrower’s productive use of capital rather than to a government subsidy.

In this structure, the bond’s sustainability depends on familiar credit-market principles:

- the borrower’s ability to generate revenue;

- the quality and liquidity of collateral;

- the term and repayment structure;

- the risk premium demanded by investors;

- and the economic usefulness of gold to the borrower.

This makes the gold bond more financially durable.

Gold bonds work best when gold is working.

India’s Sovereign Gold Bond program demonstrated that investors value both gold exposure and the opportunity to earn a return.

However, it also highlighted the limitations of a model that depends on government support rather than productive deployment of gold.

At Monetary Metals, we offer a different approach.

By connecting gold investors with businesses that can put gold to work, our Gold Yield Marketplace™ creates the potential for sustainable returns generated by real economic activity.

Key characteristics of our gold bonds include:

- Principal and interest denominated in gold: Investors receive both their principal and interest in gold, not dollars.

- Backed by productive economic activity: Borrowers use gold capital to support real business operations, such as mining or manufacturing.

- Market-driven returns: Interest rates are determined by supply-and-demand, reflecting the risk-and-return profile of each bond.

- Alignment between lenders and borrowers: Both parties participate in a gold-based financial transaction rather than a fiat-based substitute.

Discover a more sustainable gold bond model with Monetary Metals

India’s Sovereign Gold Bond program demonstrated that investors want more than exposure to rising gold prices—they also want their gold to generate a return. But the program’s challenges highlighted an important principle:

The long-term viability of any gold bond depends on how that return is created.

For investors, understanding the source of yield can help distinguish between returns supported by productive economic activity and returns that rely on external support.

The difference affects sustainability and the role gold can play within a broader wealth-preservation strategy.

At Monetary Metals, we empower investors to turn their gold into a productive asset by financing real-world transactions.

Discover how you can earn a Yield on Gold, Paid in Gold™.