Have you noticed that housing costs are near record highs?

Groceries cost more than they did a few years ago.

Insurance premiums keep rising.

And retirement requires a larger and larger nest egg.

For many households, incomes may have risen but the cost of getting ahead seems to have risen faster.

This growing affordability crisis has become one of the defining financial challenges of our time. Yet, while most discussions focus on rising prices, that may not be the real problem.

Investors who want to protect their long-term financial security may benefit from asking a different question altogether:

What if the key to navigating the affordability crisis is to preserve the purchasing power behind your wealth?

The answer may change how you think about saving, investing, and even gold itself.

Please note: All content is provided strictly for general informational and educational use. This information should not be interpreted as financial advice, nor should it replace professional consultation.

What does the affordability crisis mean for your wealth?

You don’t need to be struggling to afford groceries or rent to be affected by the affordability crisis. The real danger is more subtle.

Households living paycheck-to-paycheck may immediately feel the gap between the rate at which essential expenses increase and the rate at which savings and investments grow.

For investors, it often appears more gradually.

Your portfolio statement may show gains, and your account balances may reach new highs. Yet those gains can create a false sense of progress if they fail to keep pace with the rising cost of housing, healthcare, education, or retirement.

In other words, the affordability crisis affects more than today’s budget. It affects the future purchasing power of accumulated wealth.

How serious is the affordability crisis?

The affordability crisis is serious enough that it’s affecting multiple aspects of household finances, from housing and food costs to savings and long-term financial security.

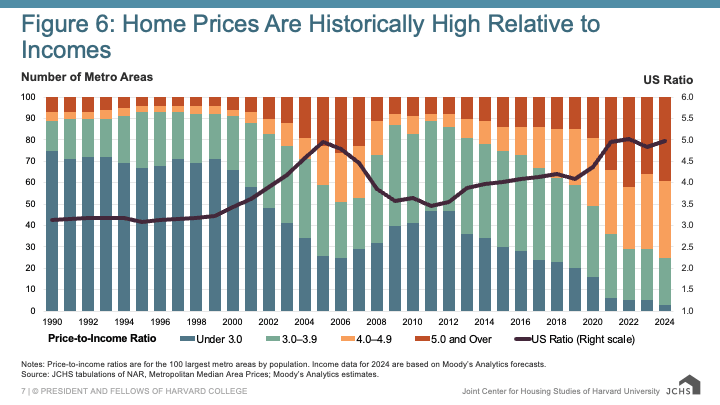

- Housing affordability is near multi-decade lows. High home prices and elevated mortgage rates have pushed home sales to their lowest level in 30 years, while record numbers of renters are considered cost-burdened1.

- Homes have become increasingly expensive relative to income. In 2024, the median existing single-family home sold for $412,500—roughly five times the median household income, well above the traditional affordability benchmark of three times income2.

- Homeownership requires more upfront capital than ever. Purchasing the median-priced home required approximately $26,800 for a minimum down payment and closing costs, or roughly $95,000 with a traditional 20% down payment2.

- Housing consumes a growing share of household income. In late 2025, a family earning the national median income needed 34% of its income to afford the mortgage payment on a median-priced new home3.

- The cost of everyday necessities continues to rise. Although inflation has slowed from its recent highs, consumer prices still increased 2.7% in 2025, while food prices rose 3.1%4.

- Americans remain concerned about rising living costs. The Federal Reserve reports that inflation—particularly the cost of food and groceries—continues to rank among households’ top financial concerns5.

The data suggest that affordability pressures aren’t a temporary inconvenience. Instead, they’re a long-term challenge that investors may need to plan for.

Traditional savings strategies may not be enough.

For generations, the standard advice was simple: save diligently, keep cash for emergencies, invest in stocks for growth, and use bonds for income and stability.

That framework still has value.

- Cash provides liquidity.

- Stocks may deliver long-term growth.

- Bonds can provide income.

- Diversification remains important.

But the affordability crisis exposes a weakness that many investors overlook: most traditional savings strategies depend on the long-term value of the dollar.

What if your money is growing but your wealth isn’t?

Many investors focus on nominal returns, but account balances don’t exist in a vacuum. If costs rise faster than your wealth, your financial position may be weaker than it appears.

This is why affordability matters to investors. More than simply accumulating dollars, the goal is to accumulate enough value to maintain or ideally improve your future standard of living.

There’s a hidden risk in cash and fixed income.

Cash feels safe because it doesn’t fluctuate the way stocks, commodities, or real estate can. A dollar in a bank account today will still be a dollar tomorrow.

Yet that stability can be deceptive. When inflation outpaces the interest earned on savings, the value of those savings gradually erodes.

The account balance may increase, but what that money can buy may decline. Bonds face a similar challenge. If the cost of living rises faster than the income your bonds generate, you can lose ground even while receiving every payment you were promised.

This is one reason inflation can be particularly challenging for conservative investors and retirees who depend on fixed-income investments.

Stocks don’t solve everything.

Stocks have historically been one of the most effective ways to build wealth over long periods, but stocks aren’t designed to solve affordability risk.

Markets can experience significant drawdowns, valuations can become stretched, and retirees may face sequence-of-returns risk if they need to withdraw assets during a downturn.

So, while stocks remain an important tool for building wealth, the challenge is that the affordability crisis isn’t simply a market problem. It’s a problem of maintaining one’s standard of living as the cost of goods and services rises over time.

For investors, this raises an important question: if traditional savings strategies may not be enough, what is?

What is the solution to the affordability crisis?

There’s no single solution to the affordability crisis.

At the societal level, the problem is complex, with economists, policymakers, builders, lenders, employers, and households all approaching the problem from different angles. While those debates matter, they’re largely beyond the control of individual investors.

At the personal level, the question is different.

You can’t single-handedly reduce national housing costs, change monetary policy, or reverse decades of price increases. But you can decide how to save, where to allocate capital, which risks to hedge, and how to measure financial success.

That means the personal response to the affordability crisis begins with a practical question:

What protects against purchasing-power risk?

Investors have several ways to address purchasing-power risk, but each comes with strengths and limitations.

- Cash provides flexibility, but little protection against long-term currency depreciation.

- Bonds provide income, but remain tied to the purchasing power of the currency in which they’re denominated.

- Stocks provide growth, but can experience prolonged periods of volatility (and they may not always outperform gold).

- Real estate can provide income and long-term appreciation, but it is often illiquid, location-dependent, and capital-intensive.

- Commodities can perform well during inflationary periods, but many are cyclical, volatile, and difficult for individual investors to own directly.

Gold is different.

How does gold preserve purchasing power?

Gold historically preserves purchasing power through monetary qualities that fiat currencies don’t possess.

- It’s scarce, durable, divisible, and widely recognized.

- It’s difficult to produce in large quantities.

- It doesn’t rely on a central bank, government, or corporation to maintain its existence.

- It’s not another party’s liability.

- It doesn’t depend on a company’s earnings or a borrower’s ability to repay.

- It has served as money across civilizations.

- It remains widely recognized as a monetary asset today.

Unlike dollars, gold can’t be printed.

Fiat currencies can be created through monetary and fiscal systems, and their supply can expand significantly over time. By contrast, gold’s supply grows slowly because it must be mined, refined, and brought to market.

Total gold supply increased just 1% in 2025, even during a year of elevated gold prices. Mine production grew only fractionally to a new record of 3,672 tonnes, while recycled supply rose 3%6.

The contrast between gold’s slow supply growth and the expansion of the money supply is one reason many investors view gold differently from fiat currencies.

Gold’s value isn’t limited by borders.

Gold is bought and sold around the world. Central banks hold it as a reserve asset, and investors use it as a hedge during periods of uncertainty. Jewelry, technology, investment, and official-sector demand all contribute to a diverse global market.

While explaining why central banks buy up gold, we described gold as a highly liquid, diversifying asset that lacks counterparty risk, boasts global demand, and is politically neutral.

This may be why many investors have often viewed gold as a long-term strategic asset rather than a short-term trade.

Every investment involves tradeoffs.

Gold shouldn’t be seen as a perfect solution or a replacement for every other asset.

- Its dollar price can move sharply.

- It may underperform stocks during strong equity bull markets.

- It may require insurance, storage, and associated costs that can vary.

Perhaps worst of all, gold’s biggest limitation has traditionally been that it couldn’t generate income.

Many investors have always accepted this tradeoff as the cost of owning a monetary asset. Its primary role was to preserve purchasing power over long periods, especially during periods of currency debasement, elevated inflation, or financial uncertainty.

That’s sufficient for maintaining wealth, but most investors seek to compound theirs.

So it seems that the key to hedging against the affordability crisis is to find a way to earn additional income in an asset that has historically maintained its value…

What if gold could be productive?

In recent decades, a new category of investment has emerged that seeks to address gold’s historic limitation: gold fixed income products.

Rather than treating gold solely as a passive store of value, these products seek to put gold to productive use while maintaining exposure to the metal itself.

How gold yield may help you navigate an affordability crisis

Gold fixed income combines two ideas that have traditionally been separate:

- Ownership of gold

- Income generation

Historically, investors often faced a choice between assets designed to preserve wealth and assets designed to generate income.

Gold occupied the first category, while bonds, dividend-paying stocks, and real estate occupied the second. Gold fixed income products seek to bridge that gap.

Preserve exposure to gold.

Gold fixed income begins with ownership of gold.

This means investors maintain exposure to the same monetary asset that many people use to diversify currency risk and hedge against inflationary environments.

The objective isn’t to replace gold ownership, but to build upon it.

Earn income without selling your gold.

Traditional gold ownership presents a challenge: an investor may benefit if gold appreciates, but generating cash flow often requires selling some of the position.

Gold fixed income products aim to create a different outcome.

Instead of reducing gold holdings to generate income, investors may be able to increase their gold holdings over time through gold-denominated yield payments.

Selling an asset produces a one-time result. Growing an asset can produce a compounding result.

Think beyond dollars.

Most investment income is denominated in fiat currency.

- Bond coupons are paid in dollars.

- Savings accounts pay interest in dollars.

- Rental income is generally collected in dollars.

Gold fixed income introduces a different framework: income is earned in gold rather than in the currency being measured against it.

For investors concerned about the long-term value of fiat currencies, this can provide a different way of thinking about wealth accumulation.

The power of compounding in gold.

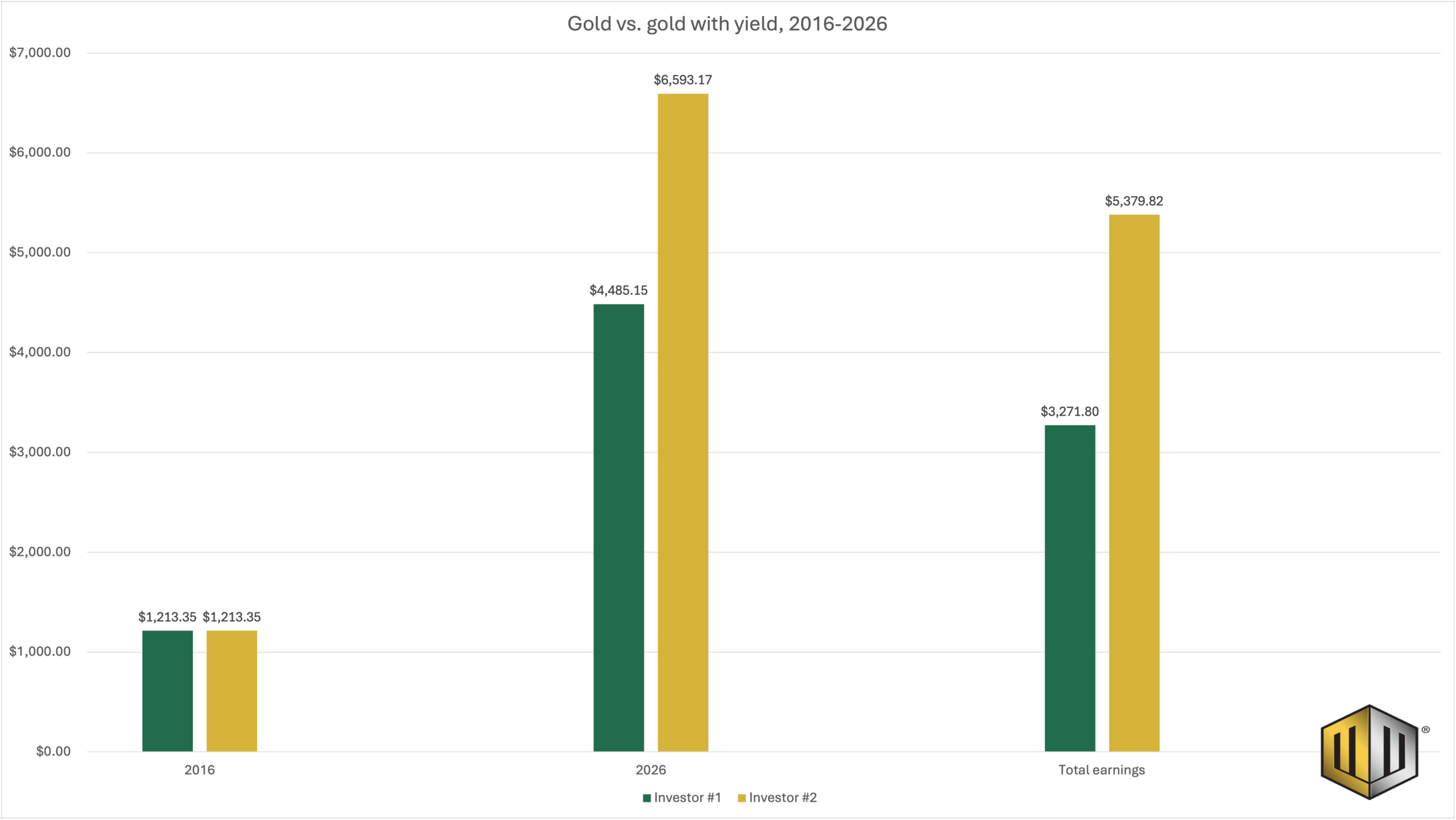

Consider two hypothetical investors who each purchased 1 ounce of gold ten years ago, investing $1,213.35, the price of gold per ounce on June 1, 20167.

The first person simply held their gold. The second invested the same gold into a gold fixed income product and reinvested all yield.

Both investors benefited from any increase in the gold price, but the second also accumulated additional ounces along the way.

The result?

The price of gold on June 1, 2026 was $4,485.15 per ounce7.

- Investor #1 still has 1 ounce of gold, so they’ve earned $3,271.80.

- Investor #2 now has 1.47 ounces of gold, so they’ve earned $5,379.82*.

*Assuming an annualized yield of 3.93%, the current weighted average return on gold in our leasing program.

This means that, even though each of their dollars buys less than it did 10 years ago, hypothetical investor #2 still has $2,108.02 more to work with—and with no additional effort on their part (short of opening an account, of course)!

Evaluating your affordability risk: 6 questions to consider

- Are your savings growing faster than your future expenses?

- How much of your wealth depends on the long-term value of the dollar?

- Do your investments generate income in assets that maintain their value?

- Have you considered how inflation affects your retirement goals?

- Are you measuring success by the size of your portfolio, or by what that portfolio can actually buy?

- If the cost of retirement doubled over the next 20 years, would your current strategy still get you there?

Hedge against the affordability crisis with Monetary Metals

The affordability crisis is often discussed in terms of rising prices, but it may be more useful to think of it as a question of preserving wealth over time. Housing, healthcare, food, education, and retirement all become more expensive over the long run.

The question is whether savings and investments can keep pace. Traditional assets continue to play an important role, but each has limitations when measured against the long-term difficulties of maintaining purchasing power.

Therefore, if the problem with affordability is that dollars buy less over time, then an asset outside the fiat currency system may provide a useful hedge. And yet, in the past, gold couldn’t generate additional income the way that traditional strategies generally could.

In 2016, Monetary Metals started challenging that outdated misconception directly. To discover how you can potentially compound your wealth in the midst of an affordability crisis, explore the benefits of opening an account today.

Sources:

- https://www.jchs.harvard.edu/state-nations-housing-2025

- https://www.jchs.harvard.edu/sites/default/files/reports/files/Harvard_JCHS_The_State_of_the_Nations_Housing_2025.pdf

- https://www.nahb.org/news-and-economics/press-releases/2026/03/affordability-posts-mild-gains-in-second-half-of-2025-but-crisis-continues

- https://www.bls.gov/opub/ted/2026/consumer-price-index-2025-in-review.htm

- https://www.federalreserve.gov/publications/2025-economic-well-being-of-us-households-in-2024-overall-financial-well-being.htm

- https://www.gold.org/goldhub/research/gold-demand-trends/gold-demand-trends-full-year-2025

- https://www.investing.com/currencies/xau-usd-historical-data