Updated: May 14, 2026

This article was first written on May 14, 2018. Eight years later, the questions that inspired this piece feel even more urgent. With inflation, debt burdens, and concerns about long-term purchasing power still shaping investor behavior, we thought it was the right time to revisit the difference between speculating on gold and investing it productively.

Investors face a challenging environment. Decades of falling interest rates force them to choose between earning poor returns in bonds and speculating on asset prices.

For much of the past two decades, falling interest rates encouraged investors to move away from income-producing assets and toward speculation on rising asset prices. Although today’s higher-rate environment has improved nominal yields, concerns about preserving purchasing power remain.

Retirees may not be able to sustain their lifestyle. Institutions may not be able to remain solvent. In addition, debt levels have skyrocketed, and there is a growing risk of default. To address these challenges, many people look for safety by buying gold or other hard assets.

Interest rates have risen in the last eight years. However, concerns about inflation, debt burdens, financial-system stability, and long-term purchasing power continue to drive investor interest in gold and other hard assets.

Dollar profits on gold investments feel like protection for your portfolio. But this way of thinking confuses investing in gold with gold investing.

What’s the difference? Below, we examine the traditional approach—then introduce a different way to think about gold ownership.

Investing in gold: Buy it and hope the numbers go up.

In general, investing in gold refers to buying the metal—but once purchased, that metal just sits in a vault. Warren Buffet humorously described this:

“Gold gets dug out of the ground in Africa, or someplace. Then we melt it down, dig another hole, bury it again and pay people to stand around guarding it. It has no utility. Anyone watching from Mars would be scratching their head.”

In “Investing in Gold,” Investopedia evaluates gold primarily through the lens of price performance relative to other assets:

“Gold has underperformed compared to the S&P 500 in the 10-year period ending Jan. 26, 2018… however, gold trounced the S&P 500 in the 10-year period from November 2002 to October 2012, with a total price appreciation of 441.5%, or 18.4% annually.”

Recent market performance illustrates that the relationship between gold and equities remains cyclical rather than one-directional. Since 2018, gold outperformed the S&P 500 in 2020, 2022, 2024, and 2025 (based on calendar-year returns), despite strong equity performance in several intervening years.

Each new gold buyer hopes that the dollar price of gold will go up. Armed with fresh capital and patience, they take over the same gold trade from the seller.

The previous investor is getting out because the price of gold has gone up enough, gone down too much, or hasn’t gone anywhere. It’s an endless cycle of churn, with each investor buying gold to try to make a buck.

The perverse logic of gold speculation

Gold speculation is a bet on the decline of the official currency. Some gold analysts go so far as to cheer for each potential new calamity in the news, with headlines declaring how a US government debt default, or a war with North Korea (or with Iran), would be “good for gold.”

Most people don’t want to bet on the price action, much less see a collapse. This is why investing in gold is not popular in the mainstream.

While gold ownership has become more mainstream in recent years through ETFs and broader investor adoption, many investors still prefer conventional income-producing assets over holding gold itself.

In any case, this isn’t really investing, as investing finances a productive activity. By contrast, gold trading is speculating: it finances nothing, and the profit comes from the capital of the next speculator.

Speculation is a zero-sum game, the process of converting one party’s capital to another’s income.

Gold investing: An ecosystem that enriches everyone.

In contrast to speculation, gold investment enriches everyone. The entrepreneur uses the gold capital to grow a profitable business, the investor earns a return on their money, and the consumer benefits from new goods and services.

Gold investing isn’t about selling one’s gold any more than conventional dollar investing is about selling one’s dollars. And as with conventional dollar investing, gold investing deploys capital into a business to increase production and grow profits.

The difference is that the capital is gold, kept on the books and payable to the investor in gold. The amount of gold paid to the investor is determined based on the amount of gold invested and the agreed rate of return.

For example, a 100oz investment at 4% yields four ounces of gold per year. The payment doesn’t depend on the price of gold; it’s not a set dollar amount, and the enterprise is using gold productively rather than simply buying gold to hold it.

This provides an advantage that dollar investing simply cannot match.

One advantage to the investor is that the yield on gold investments is not subject to any government interest-rate manipulation. When governments drive their respective currency to near-zero interest rates, this affects the yield of every currency-denominated investment.

Gold yield is not subject to monetary policy. Gold investors are getting a fair rate set in a free market, unlike dollar investors who may get little return for the risks.

The difference between holding gold and growing gold

It makes sense to hold gold as insurance against unexpected events or expenses (similar to holding physical cash).

While fewer people rely on physical cash in everyday life today, many investors still value holding some assets outside the banking and financial system as a form of financial preparedness and liquidity.

However, gold held at home doesn’t grow—storing your gold is not a long-term wealth accumulation strategy. Gold is money, and you can’t become rich by merely holding the money you already have.

That’s why we offer gold investments.

At Monetary Metals®, we offer products that provide a Yield on Gold, Paid in Gold®.

Those who invest in gold look at the price, which indicates how many dollars they’ll be paid to get rid of their gold. Alternatively, gold investors look at the gold interest rate, which indicates how much their gold will grow—in additional ounces—every year.

Any bullion dealer can exchange your 100oz of gold for $131,000*. At Monetary Metals®, our gold fixed income investments can give you 2.5oz of gold yield.**

Any bullion dealer can exchange your 100oz of gold for $465,829.† At Monetary Metals®, our gold fixed income investments can give you 3.95oz of gold yield.‡

Become a gold investor at Monetary Metals

Gold has long served as a form of financial insurance—an asset people turn to in times of uncertainty, inflation, and declining confidence in conventional markets. But simply holding gold and hoping its dollar price rises is not the same as investing it productively.

Traditional “investing in gold” often depends on speculation about future price movements. Gold investing, by contrast, focuses on growing your gold holdings over time through earned yield paid in gold itself.

For example, had you invested 10 ounces of gold in 2018 at an average annualized yield similar to today’s active leases, you’d now hold approximately 13.6 ounces.

Explore the benefits of opening an account today.

*The price of gold, as of May 14 2018, was $1,310 per ounce.

**The net yield to clients on Monetary Metals’ latest deal, as of May 14 2018, was 2.5%.

†The price of gold, as of this writing (May 14, 2026), is $4,658.29 per ounce.

‡The weighted average return in gold of all active leases at Monetary Metals is 3.95%, annualized, as of May 14, 2026.

In 2020, we issued our first gold bond. The weighted average return in gold of all active leases and bonds at Monetary Metals is 5.08%, annualized, as of May 14, 2026.

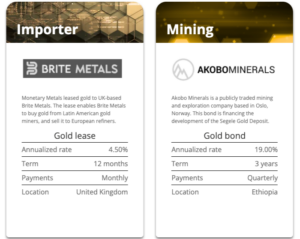

Review our funded deals for more information.

What you fail to acknowledge is that interest on any investment should reflect not only the time value of money but the risk, however small, of default. Gold holders eschew any interest in order to complete eradicate any risk of default. Your investments contain a risk of default. Always. Always. Always. The dishonesty of anyone who fails to acknowledge this risk is that they focus the investor’s gaze on the positive POTENTIAL returns, never on the potential loss of some or all of their investment.

Hold physical gold only, if you want a guarantee. Failure to do so will mean you have only yourself to blame if you lose money.