Alan Greenspan was Chairman of the Federal Reserve from 1987-2006. He died on June 21, at age 100. Rest in Peace, Mr. Greenspan.

60 years ago, he wrote an essay called “Gold and Economic Freedom.” He argued that gold protects people from confiscation of their wealth via inflation, and that gold is hated by welfare-statists because it limits the government’s ability to print money to pay for unlimited handouts. Ayn Rand published it in her book Capitalism: The Unknown Ideal.

Back then especially, it needed to be said. Millions of people have read it.

From gold advocate to Federal Reserve chairman

The only odd thing about it is that it was written by a man who was to become not just any random bureaucrat, but the Bureaucrat in Chief of the most important central planning agency in the US government.

Yes, it’s true. The Fed is a central planner that attempts to manage the economy via what’s called monetary policy. This is the idea that the central planners know the right rate of growth, the right rate of inflation, and the right number of people who are to be structurally unable to find a job—and they have just the lever to manipulate all of these numbers. Monetary debasement. In other words, the Fed inflicts the very wealth confiscation about which Greenspan wrote, in 1966, prior to taking the helm of the Federal Wealth Confiscator.

Of course there is no right rate of confiscation nor are there right rates of inflation and unemployment. And equally of course, there is no magic lever by which anybody could control monetary debasement to achieve a particular level of inflation or unemployment.

Yet this is precisely the Fed’s legislatively mandated job.

The making of “The Maestro”

The path which led a man with ideas so inimical to the Fed, to become its chairman, is a story for another day. I understand that he told the queen of free markets—Ayn Rand—that he intended to dismantle the Fed from the inside. And I assume he was sincere, in the beginning. Unfortunately, such enormous power is corrupting as JRR Tolkien so poignantly illustrates with the One Ring in his famous trilogy. Boromir was initially sincere in his desire to use the Ring to defeat Sauron, too.

During Greenspan’s two-decade tenure he was appointed by both a Democrat president and Republican presidents. He was called “The Maestro”. This is heady stuff, and one can imagine that anybody could get caught up in it, believing in his own genius, wisdom, infallibility, and incorruptibility.

Was Greenspan really “The Maestro”?

Before we look into this Maestro business, let’s review the data during his tenure.

Inflation (as measured by the Consumer Price Index) was in mostly a downward to sideways trend during his tenure, other than the spike during his first few years. So that’s good, right? Most people assume he did his job competently.

Unemployment is a bit more mixed, with two long rising periods of rising, but also seems to be overall in a downward trend across Greenspan’s two decades.

Both measures end Greenspan’s term at lower levels than they began.

These are the conventional measures by which the mainstream media, and the voters, assess the quality of a central planner. Did he make your life better, or at least make certain aggregate statistics look better?

By this standard, Greenspan is accounted the best of the best. After him, we have had controversies around Ben Bernanke, Janet Yellen, and most recently Jerome Powell (we shall see, but I suspect the new appointee, Kevin Warsh, will generate lots of controversy, too).

What sound money actually means

Greenspan was also accounted successful by a smaller group, those who care about sound money. Sound money is an odd term. It does not mean honest money. The process by which dollars are created by the Fed is not honest. The very nature of an irredeemable currency is dishonest.

Normally, a currency is a receipt of money deposited. It is, by nature, redeemable. You have the right to redeem it and retrieve your deposit. But not with the dollar. The dollar is explicitly irredeemable. It’s a promise to pay which declares that it will never pay!

Nor does sound money really mean money. “Money is gold, and nothing else,” as John Pierpont Morgan said in his Congressional testimony in 1912. The concept of money means the most marketable commodity, which was true millennia before JP Morgan’s day, and is still true today. And it means the extinguisher of debt. Payment of debt in gold is final payment. There is no further counterparty, no residual owing of anyone to anyone else. The recipient can take the metal home and put it under the mattress (or put it into a safe). Gold is no one else’s liability.

The sound money advocates don’t really even really mean “sound”. Borrowing to buy an asset is sound. Borrowing to spill cash down a welfare drain is not. The liability remains, but there is no asset. And no way to pay it off (which is also not honest).

No, none of this is what they mean by sound money. They mean consumer prices are not rising too much (whatever “too much” means).

If anything is unsound, it’s the idea of a central bank holding prices steady.

To understand why, let’s look at production and the relentless drive for more efficiency. Businesses are constantly trying to produce more stuff with fewer inputs, including land, labor, and raw materials.

Every industry from farming to high tech manufacturing, from shipping to retail distribution, from mining to refining is constantly working to improve efficiency. That is, to deliver more goods with less inputs (e.g., labor, land, raw materials, etc.)

Suppose that the average across all sectors is 2% improvement every year. Then we would expect consumer prices to be falling at around 2%. Most goods are produced in highly competitive markets, and producers can’t keep efficiency gains for very long.

But what if the Fed Chairman has a goal of 0% inflation? That would mean that he must match the rate of currency debasement to the rate of industrial efficiency gains. In this case, 2%. Assuming this were even possible, would we call it sound or honest?

No, that’s absurd. That would be a carefully measured robbery, taking from savers the benefits of the constant improvements that every industry is working so hard to generate.

Did Greenspan preserve the dollar’s gold value?

A subset of the sound money advocates is a group that thinks of the gold standard as a price-fixing scheme. According to this view, we somehow determine the right price of gold. And then the wise men at the Fed manipulate the monetary system, not with consumer prices as the target, but with the gold price as the target. If the gold price doesn’t move (too much) then they think that the fiat currency is working just like the gold standard.

According to this metric, Greenspan was a success (never mind that there is not a right price, and the Fed does not have any levers to attain any particular gold price, either).

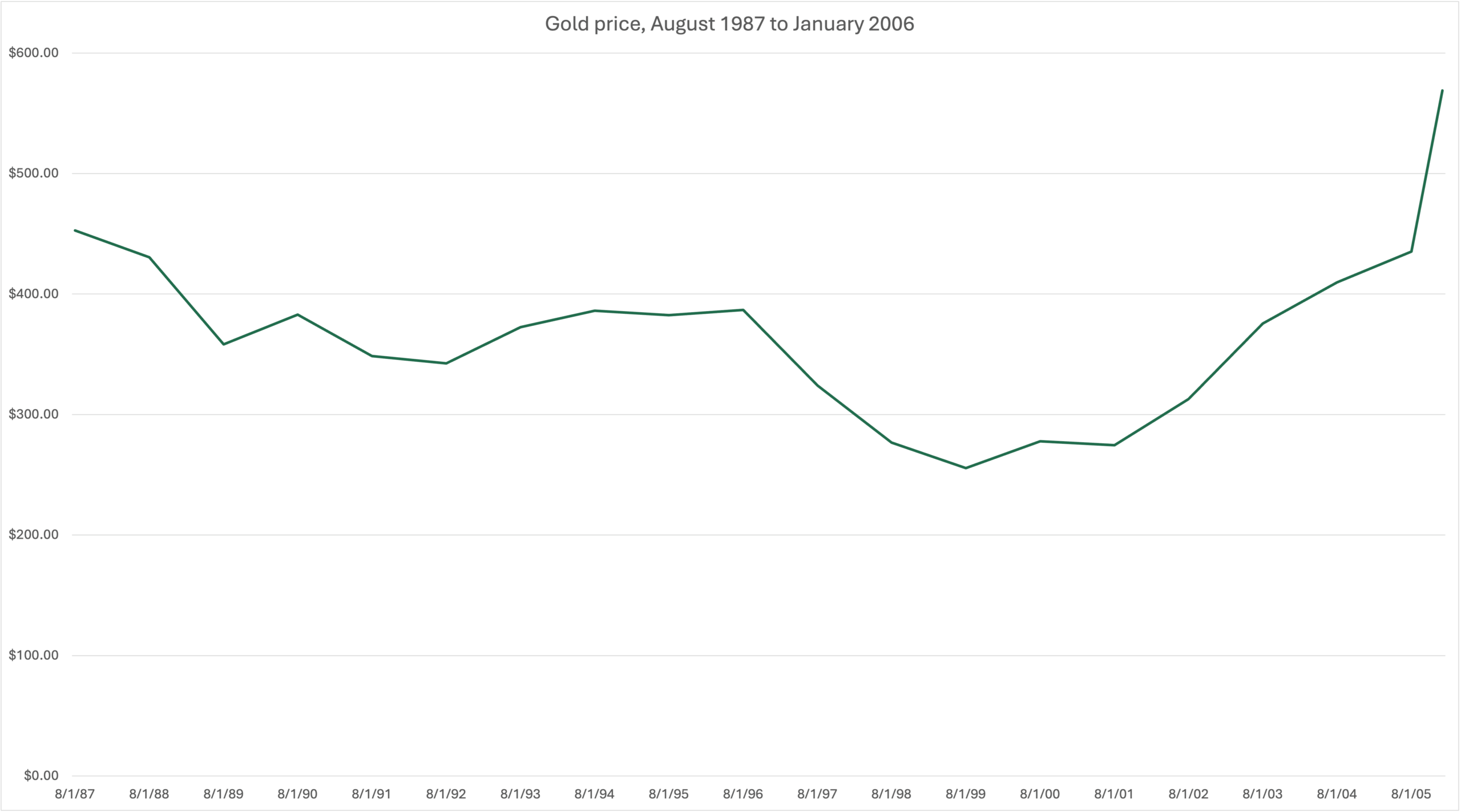

Here is a chart of the gold price during Greenspan’s tenure.

Until the bit at the end, it was a big sideways loop from a bit under $500, down under $300, then back to $500, until ending close to $600.

If one believes that the dollar can be managed, that such management is desirable, and that a central bank chief should be judged by that standard, then Greenspan was indeed The Maestro.

The hidden cost of monetary central planning

There’s just one problem.

While the Maestro encourages people to think of monetary central planning as both good and possible, it was neither. He created the conditions for stupefying amounts of unsound credit to be created to finance unsound real estate purchases, unsound currency bets around the world, and unsound business investments and acquisitions. This is the root cause of the global financial crisis of 2008.

People don’t generally blame low inflation or low unemployment, much less a steady gold price. These are taken as evidence of sound money, which is to say the money of capitalism. So, naturally, they blame capitalism for the crisis.

A central bank is no part of capitalism. It is Communist Manifesto plank #5. It is not good, even during the temporary periods wherein it seems to accomplish its stated goals. As we saw in 2008, the period of seeming stability is actually just setting the stage for a great instability.

Why honest money still matters

I am an advocate for honest money (gold). It’s not about the quantity of it. It’s not about the rate of change of consumer prices. It’s not about the number of nonworking adults.

Gold is about fair dealing, integrity, and justice. If your wage is an ounce of gold per month, then a year from now or 10 years from now, that same ounce still represents the same value for the same work. Gold has an integrity that irredeemable government promises lack. If you lend an ounce of gold and receive an ounce in return, you have been repaid on equal terms. That is justice.